Please note I am not SEBI qualified research Analyst yet.

I am feeling little better investor and stock picker after recent success of last few picks, in fact Intrasoft is biggest gainer on NSE in 2015 till June with huge difference with second and third gainer. It has already given 11 times return to me in 7 months. I should not be carried away with this success but just want to cherish this moment, sooner or latter somebody else's pick will be biggest gainer . I am still in learning phase , I need to learn lot of stuffs about picking right compounding stocks or may be multibaggers .

My new stock pick for myself which I am accumulated is Olympia Industries Ltd . It is again e-commerce play . It is profit making e-commerce play but size is still small . They have revenue of around 123 cr last year . They have reported profit of 4.57 cr against previous year's 0.36 crores (35.92 lakhs ) which around more than 1200% jump . Olympia Industries Ltd also reported revenue of 123 crores against previous years only 6 crores (around 20 times increased ). This growth is on low base so obliviously growth in percentage term will be reduce from current year .So , we can't expect something like 2000% again.Olympia Industries Ltd is Premium / Platinum Seller on Amazon . You can see their store front from the following link http://www.amazon.in/s?marketplaceID=A21TJRUUN4KGV&me=A2MTUGD8XKAQL0&merchant=A2MTUGD8XKAQL0&redirect=true . If you search olympia industries ltd then Google shows another Olympia industries page . Their correct website is http://www.olympiaindustriesltd.com/

History : Olympia Industries Ltd went into BIFR in 2001 and scheme was sanctioned in 2012 . Olympia Industries was discharged from from the sick industries' company vide BIFR Order dated 23 December 2013 by Board for Industrial and Financial Reconstruction (BIFR). Historically, the company started with manufacturing of Dyed and Blended yarns in Gujarat and Maharashtra. Presently with the company’s state of art technology and its insurmountable passion for excellence the company is now spreading its wings in Marketing & Promotion of Baby care, Home & Kitchen and Beauty & Personal Care Appliances products through E commerce on Amazon . They call them self FNFG E commerce player .

What is special ?

You will say what is special about Olympia Industries Ltd ? We already seen growth in revenue and profit . Secondly, it is profit making e-commerce company that is again rare. We already know size of opportunity in e-commerce sector , I will not go again in deep in it . It has EPS of 15 for whole year and trading on PE of around 11 and valuation of less than 40% to revenue(GMV) . These points itself speaks about good prospects of Olympia Industries Ltd . But there are lot more that makes it very attractive bet .

Along with Narayan Murthy' CloudTail, Olympia Industries Ltd is also Platinum Seller on the world’s largest Online retailer Amazon . As per unconfirmed reports CloudTail contributes around 8% to GMV of Amazon India while Olympia Industries Ltd contributes around 2.5% . Cloudtail is a 49:51 joint venture between Amazon Asia and Infosys founder NR Narayana Murthy's personal investment vehicle Catamaran was forged in last summer (2014). If Olympia Industries Ltd continues good growth and archive some scale then some other big investor can consider to invest in it . Already , Azim Premji , Narayana Murthy and Ratan Tata invested in e-commerce . http://profit.ndtv.com/news/industries/article-flipkart-amazon-battle-pits-murthy-against-premji-641274 .

If FDI in e-commerce is allowed then it will be hot cake since foreign player eyeing this type of companies , if no FDI then domestic big player will have their eye on it .

Interestingly , CloudTail has more scale of operation but customer feedback of Olympia Industries Ltd is quite better .

http://www.amazon.in/gp/aag/main?ie=UTF8&asin=&isAmazonFulfilled=1&isCBA=&marketplaceID=A21TJRUUN4KGV&orderID=&protocol=current&seller=A14UQ4H17XUX90&sshmPath=

Cloudtail Feedback

Olympia feedback

Olympia feedback

We see lot of negative comments in feedback section since more than 90% unsatisfied buyer express their feeling through negative comments . Only 10-20% satisfied buyer express their felling by positive comments and rest don't provide any feedback.Above table consider buyer as positive if the don't provide feedback . Negative percentage 1% or 2% is on total number of transactions done by seller . But if we go in comments details we see lot more negative comments than these percentage indicates.

We see lot of negative comments in feedback section since more than 90% unsatisfied buyer express their feeling through negative comments . Only 10-20% satisfied buyer express their felling by positive comments and rest don't provide any feedback.Above table consider buyer as positive if the don't provide feedback . Negative percentage 1% or 2% is on total number of transactions done by seller . But if we go in comments details we see lot more negative comments than these percentage indicates.

Group 'P' :

Since, initially company was in yarns manufacturing and went into BIFR due to accumulated losses in 2001 that time most of the shares were in physical format and BIFR scheme was sanctioned in 2012 that is after 11 years . So , most of the investor didn't converted stock from physical to demat . I suspect some of the investors might have lost physical shares paper .

SEBI has started new group P last year where Public shareholding is less than 50% in demat form.

http://www.bseindia.com/markets/MarketInfo/DispNoticesNCirculars.aspx?Noticeid={C04B49EF-9C38-4A7E-A608-5A01CCDFD3CB}¬iceno=20140827-27&dt=08/27/2014&icount=27&totcount=30&flag=0

So, according to new rule at least 50% of Public shareholding should be in demat form in order to change the group and lot of the Company at BSE.

Till March 2015 only 95335 shares of general public out of 1195215 shares were in dematerialized format.

This year NSDL has also started dematerialized process so this year we will see significant increase in dematerialized shares .

http://olympiaindustriesltd.com/img/investor-relations/sharholders/share-holder-Info/dematerialisation-of-shares.pdf

https://nsdl.co.in/downloadables/NSDL-Updates/NSDL%20Update%20-%20February%202015.pdf

Till that time it will be traded in P group with Market lot of 100 shares , it means we can buy only 100 , 200 or 300 and so on shares . We can not buy odd shares like 60 etc .

Top of that most of the brokerage houses do not allow to buy in P group example ICICIDirect don't allow to buy it.

Float :

Olympia Industries Ltd call them self as FNFG e-commerce player . Good quality FNFG player like HUL enjoys float (Other People Money ) and high return on capital employed. Similar to other FNFG players Olympia Industries Ltd also enjoy good amount of float and has reasonably good ROCE for year 2014-15.

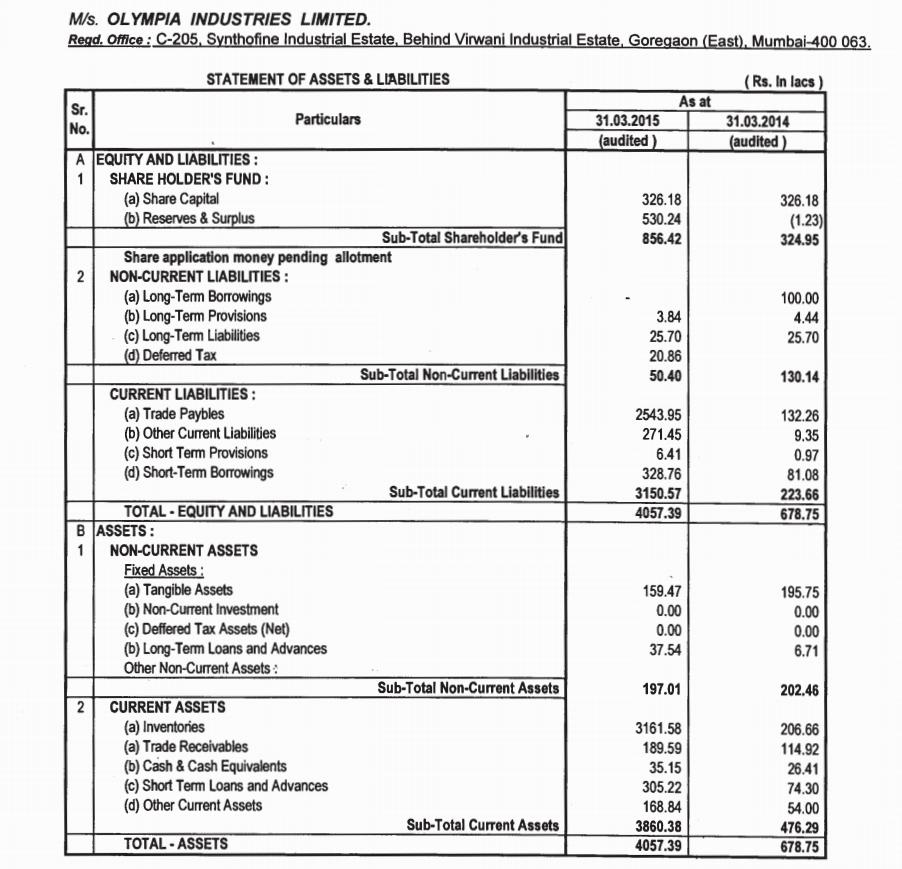

Most of the e-commerce seller worldwide don't make much money because of high inventory model . Olympia Industries Ltd also has high inventory level but that get compensate by high Trade Payable which is quite similar to HUL . No doubt HUL is quite big quality player and not comparable with Olympia Industries Ltd but I want make a point that Olympia Industries Ltd on similar path . Olympia Industries Ltd in his second innings doing some good think like venture in e-commerce that too FNFG . They are able to run their business on other people's temporary money by obtaining trade credit from their vendors . Let see statement of Assets & Liabilities for 2014-15 .

Now check Professor Sanjay Bakshi sir said about float .

https://fundooprofessor.wordpress.com/2012/08/12/flirting-with-floats-part-iii/

In brief as per Bakshi sir company can enjoy float either by advances from customer or good amount of trade payable that can compensate inventory plus trade receivable .

Total shareholder fund is 8.56 and short term borrowing is 3.28 and total equity and Liabilities is 40.57

So company enjoys float of 40.57 - 8.56 - 3.28 = 28.73 crores

Company has inventory of 31.61 and trade receivable of 1.89

31.61 + 1.89 = 33.5 against float of 28.73 .

So they just need get finance for 33.5 - 28.73 = 4.77 crores .

So , they are enjoying float of almost 85% which is going to improve in coming years . They are enjoying float more than other good companies like Symphony etc . If I get time on this weekend then I will try to compare with some small cap good stocks like Nesco , Poddar Developers Ltd etc and update this post.

It is also nicely explained at

http://www.tankrich.com/2014-40-evaluating-moats-floats/

Moat :

If a company enjoys float then there is obliviously good chance of moat . In case of Olympia Industries Ltd they do have high trade payable by obtaining trade credit from their vendors . Why vendors are offering trade credit ? Obviously vendor know capability of Olympia Industries Ltd and their track record . E-commerce is again new channel for them to increase their revenue so it is obviously win-win situation for both . They can't offer trade credit to everybody .

Olympia Industries Ltd biggest premium seller on Amazon India after Narayan Murthy's CloudTail .

Olympia Industries Ltd enjoys good moat on Amazon India platform . I can't say it is unbreakable strong moat but it is reasonably good moat .

Amazon India or any market place search engine has their own rulesets which helps bigger player to become more bigger . When user search a product then displayed search result based on lot of rules few of them are

1. Status / Ratting of seller (premium seller get preference )

2. Total Numbers of order(All) processed by seller

3. Searched product sold by sellers.

4. Of course price ( Bigger player has volume advantage for price)

etc

It is quite difficult for new small player to show their listing at top so bigger become more bigger (positive feedback loop) .

Whenever Market places go for big day sales then they depend on big premium seller instead of small sellers .

Power of sequential Multibaggers :

People says compounding is eight wonder of the world , I would say in investing world sequential Multi baggers are first wonder .

Let me explain .......

My investment of Rs 1 in kaveri in Aug 2012 ( Post on kaveri seeds) turn out to be Rs 5.5 in dec 2014 ( I had sold my 50% holding in kaveri and invested that in Intrasoft) . Now that Rs 5.5 become around 60 (11 times) this month(July 2015) in Intrasoft (Post on Intrasoft ) and Kaveri seeds is hovering below my sold price (Although , I still hold few shares of Kaveri). I have sold my holding of 12% from Intrasoft (avg price around rs 540 , against my avg of Rs 48 ) and invested that in Olympia Industries Ltd . I still believe Intrasoft will grow much faster than Olympia in coming years but I had to invest something in Olympia Industries Ltd and I can't wait till next month's salary .

If by god's grace Olympia Industries Ltd double from my avg price of around Rs 158 in one year then I will have 120 baggers (1*5.5*11*2) in 4 years . That is quite significant since Raamdeo Agrawal says he has only one 100x bagger in his life i.e. Hero Motocorp . Although , He might have lot of sequential multi baggers . Lot of other senior investors of micro cap like VP sir (http://value-picks.blogspot.in/ ) ,Porinju sir , Ayush Mittal , Amit Arora etc might already have this type of 100x sequential mutibaggers but this will be my first . Fingers are crossed .

Basant sir already has explained Power of sequential Multi baggers in his book (the thoughtful investor) in his words . Must read for all Indian investors . http://www.thethoughtfulinvestor.in/

I may be day dreaming of 100 fold return in 4 years but I am same person who had to bear losses on companies like Agre developer and Chowgule etc . I have learnt lot from that point but still I need to learn lot in investing world . I can pass test only if my portfolio performs comparatively good in bear market as well.

P.S. (19 July 2015 )

Risk : They mainly depend on one market place Amazon India performance . Secondly , company came out of BIFR and playing second inning . We have seen Symphony has created wealth after company came out from BIFR but we don't know if Olympia will also create wealth for us or not . If promoter show integrity and want to share wealth with retail investor then no doubt about that it will be good wealth creator . Promoter just need to follow good corporate governance practices .

Valuation :

It is trading below PE of 12 and around 0.4 x to sales . If we compare with other listed e-commerce player even though they have different model then we can say it highly undervalued even though it has appreciated 6-7 times this year .

Intrasoft is trading on mcap to sales ration of 2.x . If Olympia Industries Ltd gets same valuation then it should have mcap of around 250 crores .

Infibeam is asking about at least 7-8 times to sales (GMV) . I don't want to speculate valuation of Olympia Industries Ltd based on Infibeam valuation .

Info Edge (India) Ltd ( Quite different e-commerce player ) is trading on 10700 cr mcap on sales of 600 crores with PE of 470 .

For me Olympia Industries Ltd has all the following ingredient which is necessity for future wealth creators or at least few baggers .

1. Large scope of opportunity

2. Among rare profitable e-commerce player

3. Enjoys high float (85% )

4. Low net working capital requirement ( around 5 crores only ) due to float .

5. High ROCE above 50 ( Most of the websites will reflect it only after annual report of 2014-15 )

6. Shown High growth , even though this June quarter or first half will subdued .

7. Non Cyclic FNFG player.

Finally what Jeff Bezos says about finding good companies , we can judge Olympia Industries after at least 3-4 years of good performance . Right now , it is too early .

I am feeling little better investor and stock picker after recent success of last few picks, in fact Intrasoft is biggest gainer on NSE in 2015 till June with huge difference with second and third gainer. It has already given 11 times return to me in 7 months. I should not be carried away with this success but just want to cherish this moment, sooner or latter somebody else's pick will be biggest gainer . I am still in learning phase , I need to learn lot of stuffs about picking right compounding stocks or may be multibaggers .

My new stock pick for myself which I am accumulated is Olympia Industries Ltd . It is again e-commerce play . It is profit making e-commerce play but size is still small . They have revenue of around 123 cr last year . They have reported profit of 4.57 cr against previous year's 0.36 crores (35.92 lakhs ) which around more than 1200% jump . Olympia Industries Ltd also reported revenue of 123 crores against previous years only 6 crores (around 20 times increased ). This growth is on low base so obliviously growth in percentage term will be reduce from current year .So , we can't expect something like 2000% again.Olympia Industries Ltd is Premium / Platinum Seller on Amazon . You can see their store front from the following link http://www.amazon.in/s?marketplaceID=A21TJRUUN4KGV&me=A2MTUGD8XKAQL0&merchant=A2MTUGD8XKAQL0&redirect=true . If you search olympia industries ltd then Google shows another Olympia industries page . Their correct website is http://www.olympiaindustriesltd.com/

History : Olympia Industries Ltd went into BIFR in 2001 and scheme was sanctioned in 2012 . Olympia Industries was discharged from from the sick industries' company vide BIFR Order dated 23 December 2013 by Board for Industrial and Financial Reconstruction (BIFR). Historically, the company started with manufacturing of Dyed and Blended yarns in Gujarat and Maharashtra. Presently with the company’s state of art technology and its insurmountable passion for excellence the company is now spreading its wings in Marketing & Promotion of Baby care, Home & Kitchen and Beauty & Personal Care Appliances products through E commerce on Amazon . They call them self FNFG E commerce player .

What is special ?

You will say what is special about Olympia Industries Ltd ? We already seen growth in revenue and profit . Secondly, it is profit making e-commerce company that is again rare. We already know size of opportunity in e-commerce sector , I will not go again in deep in it . It has EPS of 15 for whole year and trading on PE of around 11 and valuation of less than 40% to revenue(GMV) . These points itself speaks about good prospects of Olympia Industries Ltd . But there are lot more that makes it very attractive bet .

Along with Narayan Murthy' CloudTail, Olympia Industries Ltd is also Platinum Seller on the world’s largest Online retailer Amazon . As per unconfirmed reports CloudTail contributes around 8% to GMV of Amazon India while Olympia Industries Ltd contributes around 2.5% . Cloudtail is a 49:51 joint venture between Amazon Asia and Infosys founder NR Narayana Murthy's personal investment vehicle Catamaran was forged in last summer (2014). If Olympia Industries Ltd continues good growth and archive some scale then some other big investor can consider to invest in it . Already , Azim Premji , Narayana Murthy and Ratan Tata invested in e-commerce . http://profit.ndtv.com/news/industries/article-flipkart-amazon-battle-pits-murthy-against-premji-641274 .

If FDI in e-commerce is allowed then it will be hot cake since foreign player eyeing this type of companies , if no FDI then domestic big player will have their eye on it .

Interestingly , CloudTail has more scale of operation but customer feedback of Olympia Industries Ltd is quite better .

http://www.amazon.in/gp/aag/main?ie=UTF8&asin=&isAmazonFulfilled=1&isCBA=&marketplaceID=A21TJRUUN4KGV&orderID=&protocol=current&seller=A14UQ4H17XUX90&sshmPath=

Cloudtail Feedback

Group 'P' :

Since, initially company was in yarns manufacturing and went into BIFR due to accumulated losses in 2001 that time most of the shares were in physical format and BIFR scheme was sanctioned in 2012 that is after 11 years . So , most of the investor didn't converted stock from physical to demat . I suspect some of the investors might have lost physical shares paper .

SEBI has started new group P last year where Public shareholding is less than 50% in demat form.

http://www.bseindia.com/markets/MarketInfo/DispNoticesNCirculars.aspx?Noticeid={C04B49EF-9C38-4A7E-A608-5A01CCDFD3CB}¬iceno=20140827-27&dt=08/27/2014&icount=27&totcount=30&flag=0

So, according to new rule at least 50% of Public shareholding should be in demat form in order to change the group and lot of the Company at BSE.

Till March 2015 only 95335 shares of general public out of 1195215 shares were in dematerialized format.

This year NSDL has also started dematerialized process so this year we will see significant increase in dematerialized shares .

http://olympiaindustriesltd.com/img/investor-relations/sharholders/share-holder-Info/dematerialisation-of-shares.pdf

https://nsdl.co.in/downloadables/NSDL-Updates/NSDL%20Update%20-%20February%202015.pdf

Till that time it will be traded in P group with Market lot of 100 shares , it means we can buy only 100 , 200 or 300 and so on shares . We can not buy odd shares like 60 etc .

Top of that most of the brokerage houses do not allow to buy in P group example ICICIDirect don't allow to buy it.

Float :

Olympia Industries Ltd call them self as FNFG e-commerce player . Good quality FNFG player like HUL enjoys float (Other People Money ) and high return on capital employed. Similar to other FNFG players Olympia Industries Ltd also enjoy good amount of float and has reasonably good ROCE for year 2014-15.

Most of the e-commerce seller worldwide don't make much money because of high inventory model . Olympia Industries Ltd also has high inventory level but that get compensate by high Trade Payable which is quite similar to HUL . No doubt HUL is quite big quality player and not comparable with Olympia Industries Ltd but I want make a point that Olympia Industries Ltd on similar path . Olympia Industries Ltd in his second innings doing some good think like venture in e-commerce that too FNFG . They are able to run their business on other people's temporary money by obtaining trade credit from their vendors . Let see statement of Assets & Liabilities for 2014-15 .

Now check Professor Sanjay Bakshi sir said about float .

https://fundooprofessor.wordpress.com/2012/08/12/flirting-with-floats-part-iii/

In brief as per Bakshi sir company can enjoy float either by advances from customer or good amount of trade payable that can compensate inventory plus trade receivable .

Total shareholder fund is 8.56 and short term borrowing is 3.28 and total equity and Liabilities is 40.57

So company enjoys float of 40.57 - 8.56 - 3.28 = 28.73 crores

Company has inventory of 31.61 and trade receivable of 1.89

31.61 + 1.89 = 33.5 against float of 28.73 .

So they just need get finance for 33.5 - 28.73 = 4.77 crores .

So , they are enjoying float of almost 85% which is going to improve in coming years . They are enjoying float more than other good companies like Symphony etc . If I get time on this weekend then I will try to compare with some small cap good stocks like Nesco , Poddar Developers Ltd etc and update this post.

It is also nicely explained at

http://www.tankrich.com/2014-40-evaluating-moats-floats/

Moat :

If a company enjoys float then there is obliviously good chance of moat . In case of Olympia Industries Ltd they do have high trade payable by obtaining trade credit from their vendors . Why vendors are offering trade credit ? Obviously vendor know capability of Olympia Industries Ltd and their track record . E-commerce is again new channel for them to increase their revenue so it is obviously win-win situation for both . They can't offer trade credit to everybody .

Olympia Industries Ltd biggest premium seller on Amazon India after Narayan Murthy's CloudTail .

Olympia Industries Ltd enjoys good moat on Amazon India platform . I can't say it is unbreakable strong moat but it is reasonably good moat .

Amazon India or any market place search engine has their own rulesets which helps bigger player to become more bigger . When user search a product then displayed search result based on lot of rules few of them are

1. Status / Ratting of seller (premium seller get preference )

2. Total Numbers of order(All) processed by seller

3. Searched product sold by sellers.

4. Of course price ( Bigger player has volume advantage for price)

etc

It is quite difficult for new small player to show their listing at top so bigger become more bigger (positive feedback loop) .

Whenever Market places go for big day sales then they depend on big premium seller instead of small sellers .

Power of sequential Multibaggers :

People says compounding is eight wonder of the world , I would say in investing world sequential Multi baggers are first wonder .

Let me explain .......

My investment of Rs 1 in kaveri in Aug 2012 ( Post on kaveri seeds) turn out to be Rs 5.5 in dec 2014 ( I had sold my 50% holding in kaveri and invested that in Intrasoft) . Now that Rs 5.5 become around 60 (11 times) this month(July 2015) in Intrasoft (Post on Intrasoft ) and Kaveri seeds is hovering below my sold price (Although , I still hold few shares of Kaveri). I have sold my holding of 12% from Intrasoft (avg price around rs 540 , against my avg of Rs 48 ) and invested that in Olympia Industries Ltd . I still believe Intrasoft will grow much faster than Olympia in coming years but I had to invest something in Olympia Industries Ltd and I can't wait till next month's salary .

If by god's grace Olympia Industries Ltd double from my avg price of around Rs 158 in one year then I will have 120 baggers (1*5.5*11*2) in 4 years . That is quite significant since Raamdeo Agrawal says he has only one 100x bagger in his life i.e. Hero Motocorp . Although , He might have lot of sequential multi baggers . Lot of other senior investors of micro cap like VP sir (http://value-picks.blogspot.in/ ) ,Porinju sir , Ayush Mittal , Amit Arora etc might already have this type of 100x sequential mutibaggers but this will be my first . Fingers are crossed .

Basant sir already has explained Power of sequential Multi baggers in his book (the thoughtful investor) in his words . Must read for all Indian investors . http://www.thethoughtfulinvestor.in/

I may be day dreaming of 100 fold return in 4 years but I am same person who had to bear losses on companies like Agre developer and Chowgule etc . I have learnt lot from that point but still I need to learn lot in investing world . I can pass test only if my portfolio performs comparatively good in bear market as well.

P.S. (19 July 2015 )

Risk : They mainly depend on one market place Amazon India performance . Secondly , company came out of BIFR and playing second inning . We have seen Symphony has created wealth after company came out from BIFR but we don't know if Olympia will also create wealth for us or not . If promoter show integrity and want to share wealth with retail investor then no doubt about that it will be good wealth creator . Promoter just need to follow good corporate governance practices .

Valuation :

It is trading below PE of 12 and around 0.4 x to sales . If we compare with other listed e-commerce player even though they have different model then we can say it highly undervalued even though it has appreciated 6-7 times this year .

Intrasoft is trading on mcap to sales ration of 2.x . If Olympia Industries Ltd gets same valuation then it should have mcap of around 250 crores .

Infibeam is asking about at least 7-8 times to sales (GMV) . I don't want to speculate valuation of Olympia Industries Ltd based on Infibeam valuation .

Info Edge (India) Ltd ( Quite different e-commerce player ) is trading on 10700 cr mcap on sales of 600 crores with PE of 470 .

For me Olympia Industries Ltd has all the following ingredient which is necessity for future wealth creators or at least few baggers .

1. Large scope of opportunity

2. Among rare profitable e-commerce player

3. Enjoys high float (85% )

4. Low net working capital requirement ( around 5 crores only ) due to float .

5. High ROCE above 50 ( Most of the websites will reflect it only after annual report of 2014-15 )

6. Shown High growth , even though this June quarter or first half will subdued .

7. Non Cyclic FNFG player.

Finally what Jeff Bezos says about finding good companies , we can judge Olympia Industries after at least 3-4 years of good performance . Right now , it is too early .

1. Provide your email ID.

2. Check your email inbox for confirmation email and click on confirmation link.

Alternatively ,

If you are interested in reading multiple blogs from bloggers then please open your free account on http://www.feedly.com/ which I find good to read and track all the blogs .

Alternatively ,

If you are interested in reading multiple blogs from bloggers then please open your free account on http://www.feedly.com/ which I find good to read and track all the blogs .

Disclaimer : Please treat this post as starting point of your research and not conclusion to invest in any discussed stock. In fact I already invested in Olympia so my views are going to be biased . As always , please take the advice of a SEBI qualified financial adviser .